Picture Sarah, a 24-year-old landing her first office job. Bills stack up fast: rent, groceries, that daily latte. She checks her bank app and panics. Sound familiar?

Basic financial principles give you control. They turn confusion into confidence. You learn simple rules to track money, budget wisely, save for surprises, handle debt, and build good habits.

This guide covers those steps for beginners in 2026. With interest rates dropping and free apps everywhere, now’s the time. Ready to take charge? Let’s start with knowing your cash flow.

Track Your Money to Know Where You Stand

You can’t fix what you don’t see. Beginners often guess where money goes. That leads to overdrafts and stress. Start by listing all income and expenses. This builds the base for everything else.

Grab a notebook or app. Note your paycheck, side hustle cash, even birthday gifts. Then track spending: rent, gas, Netflix, snacks. A $5 coffee five days a week? That’s $100 a month. Surprising, right?

Awareness stops leaks. Set goals like saving $50 next month. Track weekly to stay on course. Free templates online let you copy a simple sheet.

List Your Income and Expenses First

Jot down take-home pay. Say you earn $3,000 monthly after taxes. Categorize expenses: needs like $1,200 rent and food; wants like $300 dining out; savings goal of $200.

Don’t skip small stuff. Subscriptions add up quick. In 2026, apps like Mint or PocketGuard link accounts for free. They flag overspending. Test one for a week.

| Category | Example Expenses | Monthly Amount ($3,000 Income) |

|---|---|---|

| Needs | Rent, utilities, groceries | $1,500 |

| Wants | Movies, coffee, clothes | $900 |

| Savings | Emergency fund, goals | $600 |

This table shows a starter split. Adjust as needed. Track one month; you’ll spot patterns fast.

Set Goals You Can Actually Hit

Vague plans fail. Use SMART: specific, measurable, achievable, relevant, time-bound. Instead of “save more,” aim to “save $100 by June 30.”

Track progress in your app. Hitting $200 saved motivates you. Beginners build to $1,000 quick. Celebrate small wins. This habit sticks.

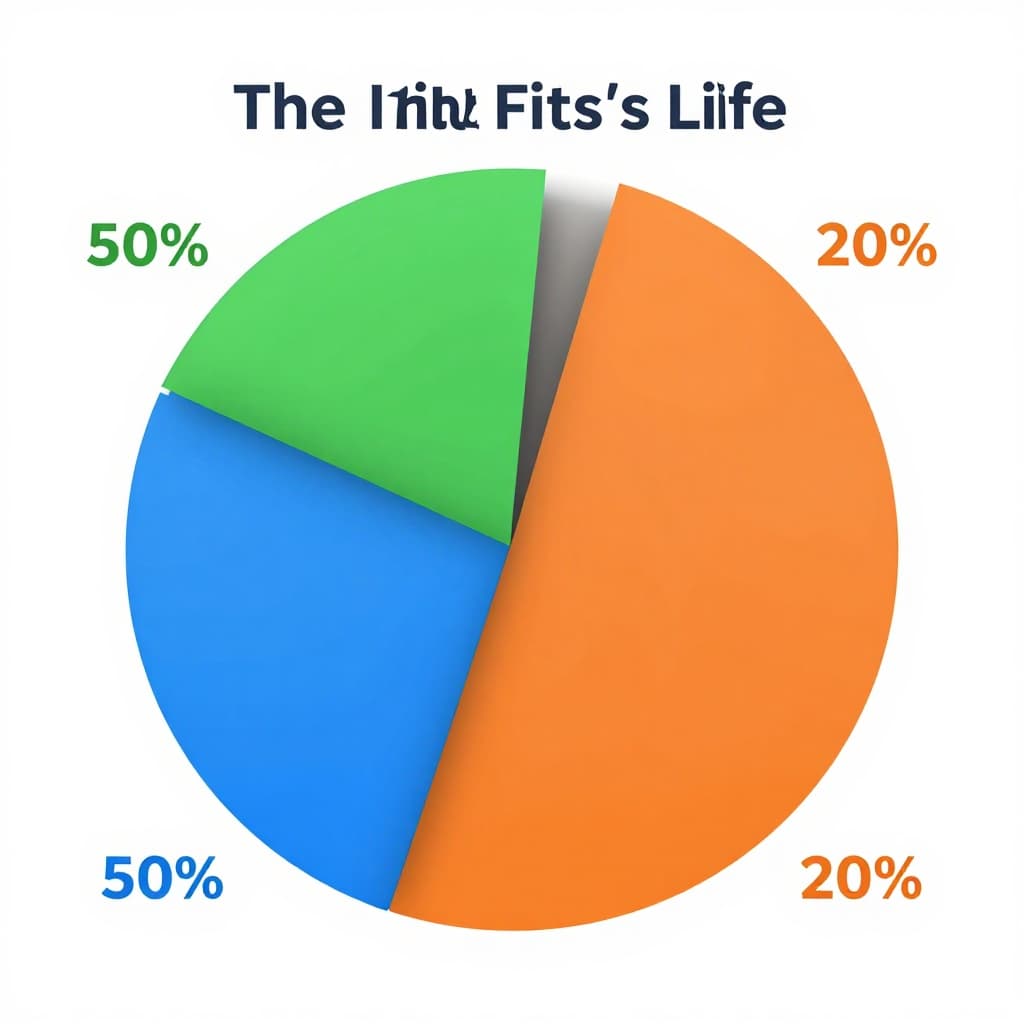

Create a Budget That Fits Your Life

A budget plans your month. It matches income to spending. No more wondering where cash vanished.

The 50/30/20 rule works great for starters. Put 50% to needs, 30% to wants, 20% to savings or debt. On $3,000, that’s $1,500 needs, $900 wants, $600 saved.

Tweak if rent eats more. Rising costs in 2026? Cut wants first. For details, check Citi’s guide to the 50/30/20 rule. Track a month to refine it.

Follow the 50/30/20 Rule for Easy Starts

Needs cover housing, food, transport: $1,500 on $3,000. Wants: entertainment, hobbies at $900. Savings: the rest.

Common mix-up? Gym fees as needs (yes, health) vs. new shoes (wants). Test it. Apps like CNBC’s top free budgeting tools make it simple. Results show quick control.

Build Savings to Handle Life’s Surprises

Life throws curveballs: flat tire, lost job. An emergency fund covers 3-6 months expenses. Start small at $1,000.

Pay yourself first. Transfer 10-20% income to savings right after payday. High-yield accounts pay up to 5.00% APY now, way above 0.39% average. See NerdWallet’s best high-yield savings accounts for March 2026.

Start Your Emergency Fund Today

Open a separate account. Save $25 weekly. Hits $1,000 in a year. Build slow; consistency counts.

Automate Savings with Pay Yourself First

Set bank transfer day after payday. No thinking needed. Builds habit fast. Federal funds rate at 3.50-3.75% means rates may dip, so lock in now.

Pay Off Debt the Smart Way

List debts: balances, rates. Credit cards hit 20%; student loans 5%. Pay minimums on all. Extra on highest rate first: avalanche method.

It saves most interest. Snowball pays smallest first for quick wins. Beginners? Avalanche wins math-wise. Compare via BuckGuru’s debt avalanche vs snowball breakdown.

Sample: $2,000 card at 18%, $5,000 loan at 6%. Avalanche clears card fast, saves $150 interest.

Tackle High-Interest Debt First

Pay $100 extra on card monthly. Clears in 18 months vs. years. Avoid new debt. Dropping rates in 2026 help refi later.

Adopt Simple Habits for Long-Term Wins

Cook meals; save $200 monthly vs. takeout. Buy bulk groceries. Skip impulse buys: wait 24 hours.

Track wins. Small changes add hundreds yearly. Stay honest. In 2026, basics beat fancy invests. Consistency grows wealth.

Master these principles, and money works for you. Track this week; pick one habit. Small steps lead to freedom.

What’s your first move? Share below, and subscribe for more tips. You’ve got this.

(Word count: 982)